After a year long Bear Market in the S&P, NASDAQ and longer than that in other subsets of the market, the drivers of the current economic malaise are becoming more evident.

There are growing signs that the drivers of this current economic disruption are identifiable. While the latest ramp likely fades again - mostly because the FED WANTS it to Fade, we may soon be entering a terminal phase of this cycle. As David Zervos, of Jeffries who is considered one of the Market Strategist closest to the FED recently told me, the FED really does not want the market to ramp again …yet. They will use rhetoric to put a cap on things if animal spirits rise up again. But there is also likely some sense of downside limit for them as well barring recession. That, however is likely lower than the old concept of the “FED Put”. So, the range is likley 3,500-4400 SP500 for a bit longer.

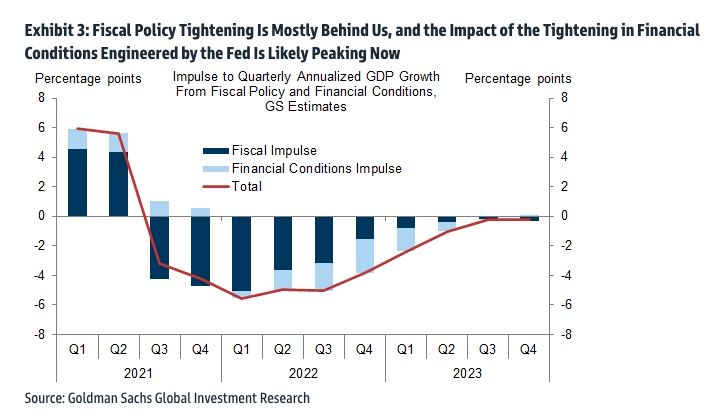

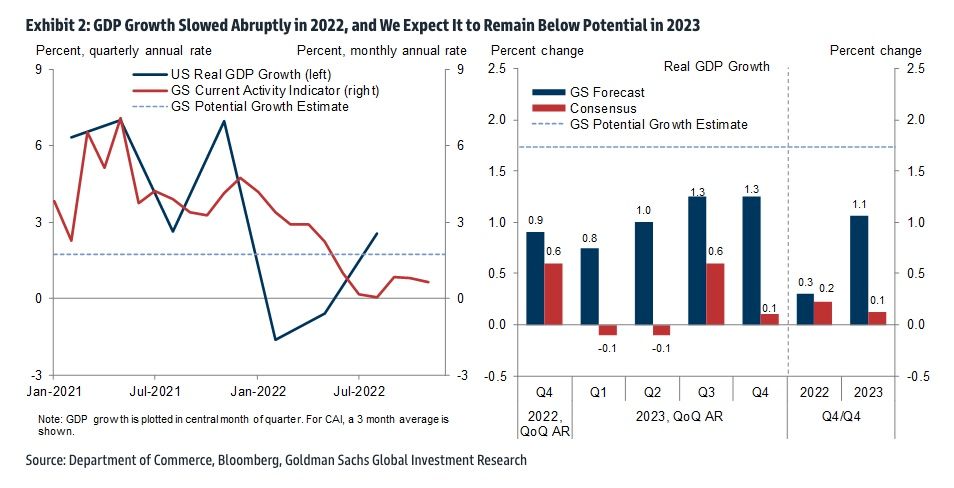

As Goldman Sachs has suggested, there is growing confidence that the bulk of the rate increases have been put in place. The FED jacked up rates at the fastest pace in history because they knew that they were a bit late (3-6 months).

So, they felt the need to “catch up”. Most of Wall Street came to believe that that speed x level would immediately cause a recession. That concept makes alot of sense. In fact, we did have negative GDP for two quarters as the FED began, in Q1 and Q2 of 2022- which in my mind is a recession. But the question arises, if those two quarters were not the recession, then ….why hasn’t it happened yet? Is it just a matter of time? Maybe, but here is another theory:

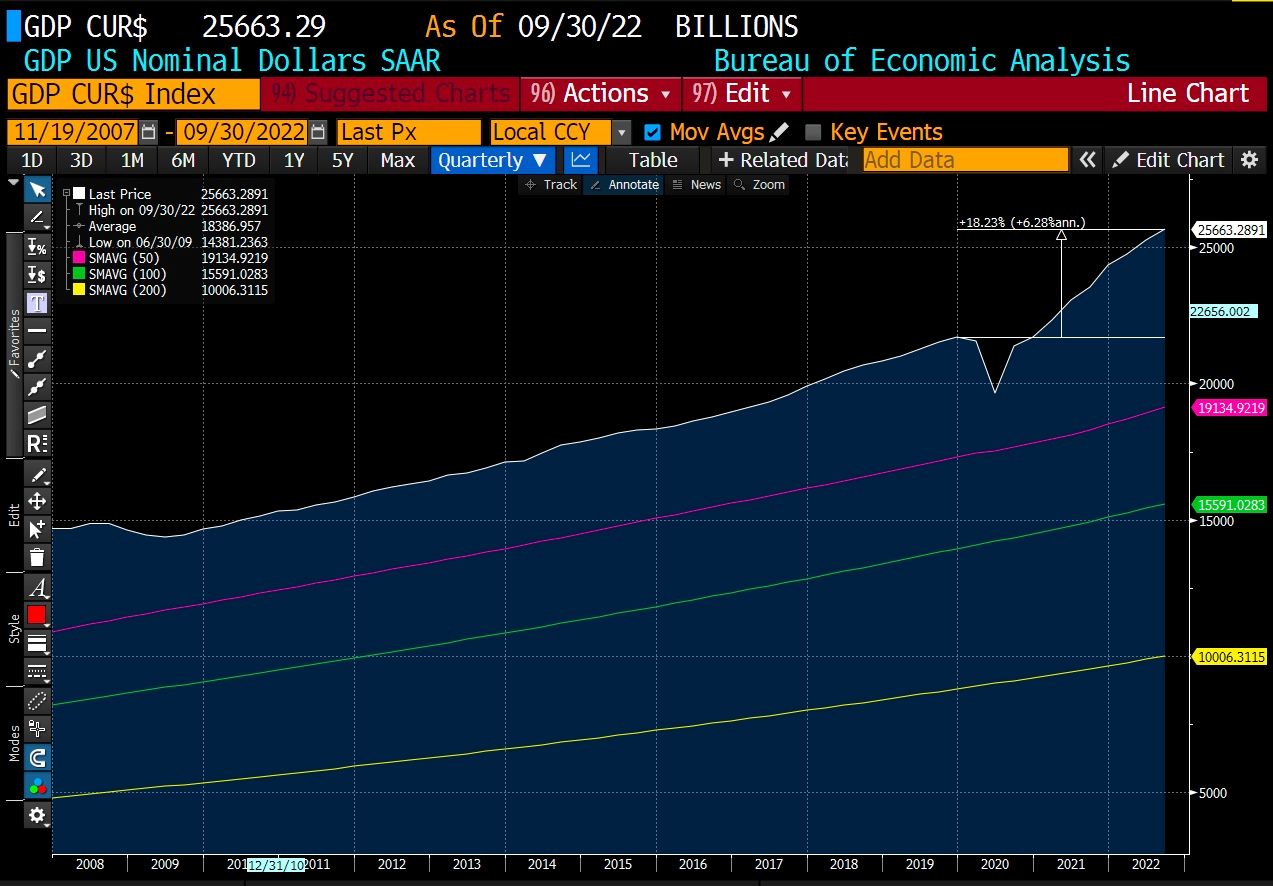

In the last two years US NOMINAL GDP has grown more than 20%. Our economy has grown from $20 Trillion to over $25Trillion....again, in just two years. That is actually one of the fastest periods of growth ever! Shocking, yes. Most do not realise this.

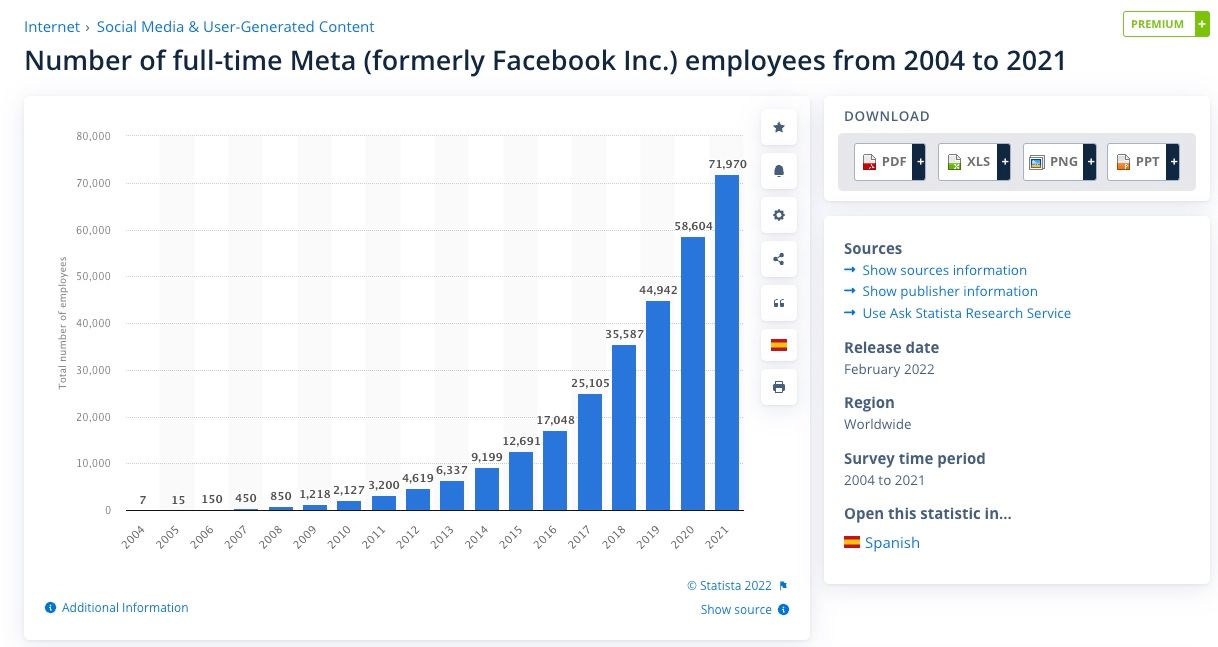

The Covid growth boom was indeed real, but also transitory. Output really has been strong as the FED has been saying. But, the COVID policies also obviously created much of the inflation we are now seeing. The idea of shutting down economies while pushing massive stimulus into the system was clearly a bad idea. Businesses that benefitted the most from the "Work from Home" phenomenon, mostly tech, grossly overestimated the durability of that mini boomlet and spent like crazy. This drove up prices for components, facilities, commodities et al. It spurred insane hiring practices and expansion plans throughout the supply chain. This seeped into most areas of the economy to varying degrees. That growth forecast was so wrong! So, now the (necessary) cutbacks are happening. In the case of Meta, which is just one of many who are realising their mistakes, just announced a massive layoff of 11,000 workers. But yet that only brings their total personnel back to a level that is get this ... still 10% higher than they had at end of 2021!

So, the result has been raging inflation. Inflation clearly creates massive challenges to families, businesses and the economy at large. But, there is some upside to businesses as the top line revenues are “supported”. We have seen for each Quarter of reported earnings this year generally better than expected sales and earnings for US corporates. According to Zervos, US earnings will not likely see the massive cliff that most expect (barring recession) because this ramp in Nominal GDP is flowing into corporate coffers. An additional benefit of inflation is that it actually helps the debt picture as it “devalues” the value of the current debt levels into the future. At the same time the US debt burden has seen a meaningful drop from 130% of GDP down to 120% and continues to trend better.

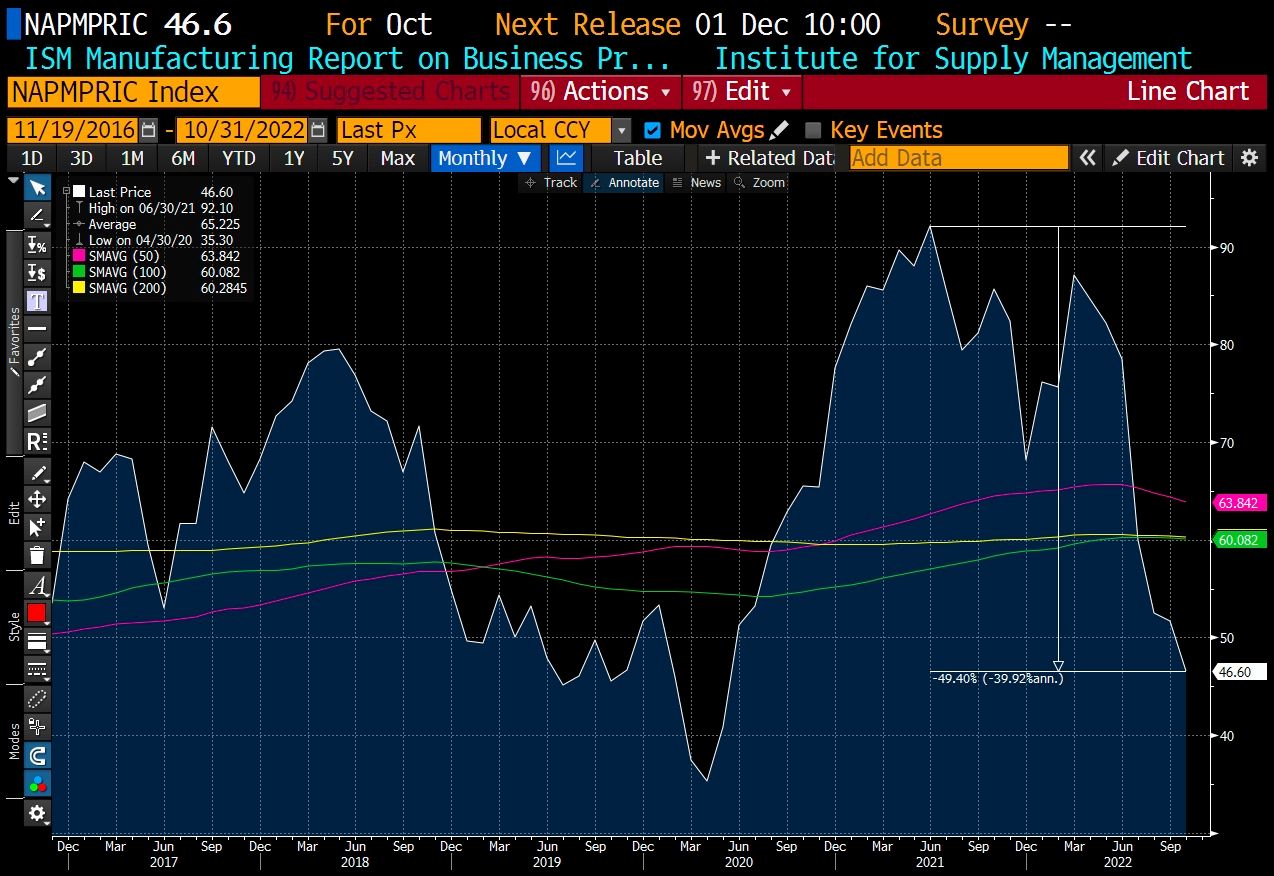

So, there is a balancing act that the FED needs to succeed at during this period. Lowering inflation while avoiding a recession - or at least a significant one. The first part of this challenge is already coming into view and trending appropriately. It is possible that the trend break in the US dollar is the first sign, as is often the case in currencies, that there is evidence that the FED is back on track. For example, many commodities have stopped their upward trends. Oil prices and Nat Gas prices are down 40%, Wheat and Corn are down 37% and 20% respectively. Copper prices are down 26%. Even in Europe, direct effects of the Ukraine war are easing a bit. In Germany, for example, baseload electricity prices are moving back down and are substantially lower than the summer peaks. The ISM Manufacturing prices paid component (graph below) is on a downward trend and has dropped 49% since the inflation peak in the summer!

So, we have input prices trending lower. In a very surprising twist, we actually have GDP estimates beginning to rise. The Atlanta FED maintains their forecasts publicly. Their latest estimate, referred to as the GDPNow is estimating US GDP at 4.18%. Most notable about this forecast is not just the strength of the number but that it has risen from negative 2% in June of this year to the current 4.18%!

So, as Goldman Sachs said this week "The initial steps along this path have been successful, but there is much further to go in 2023. We expect another year of below-potential growth and labor market rebalancing to solve much but not all of the underlying inflation problem. Unlike consensus, we do not expect a recession"

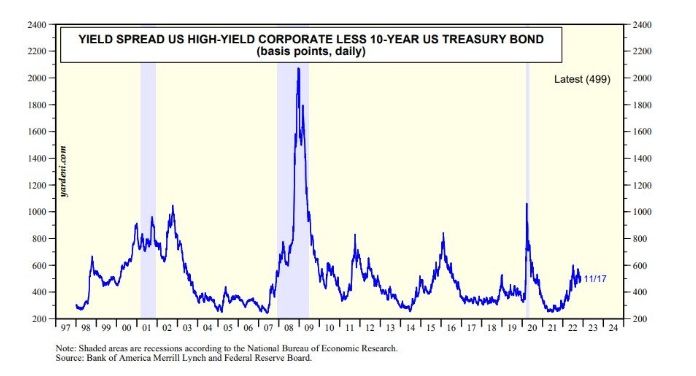

As we all know, the longer duration and deeper the depth of any Bear market, the higher the chances of bodies floating to the surface. It happened in most of the big ones, from Madoff, Lehman Brothers and LTCM to the Milken Junk Bond scandal in the 1980's. There is generally something that breaks. Is it possible that the FTX fiasco is just that "market sign" occurring again? Possible. The big question is whether this might cause a "contagion spiral". While it IS creating the expected contagion in Crypto, thus far, it has not bled over to Traditional Financial Markets. In fact, there is an argument to be made that because of the lax (no) regulation in the once $3 Trillion Crypto market, most of the bad actors focused their scams on that market - and not Traditional Finance (TradFi). This logic seems to make sense and if true is a win for Wall Street asset classes and the economy at large. But we are carefully watching all of this daily for signs of creeping market stresses. Thus far, some key indicators such as Credit spreads, Bank Loans weekly loan loss bank provisions are thus far contained:

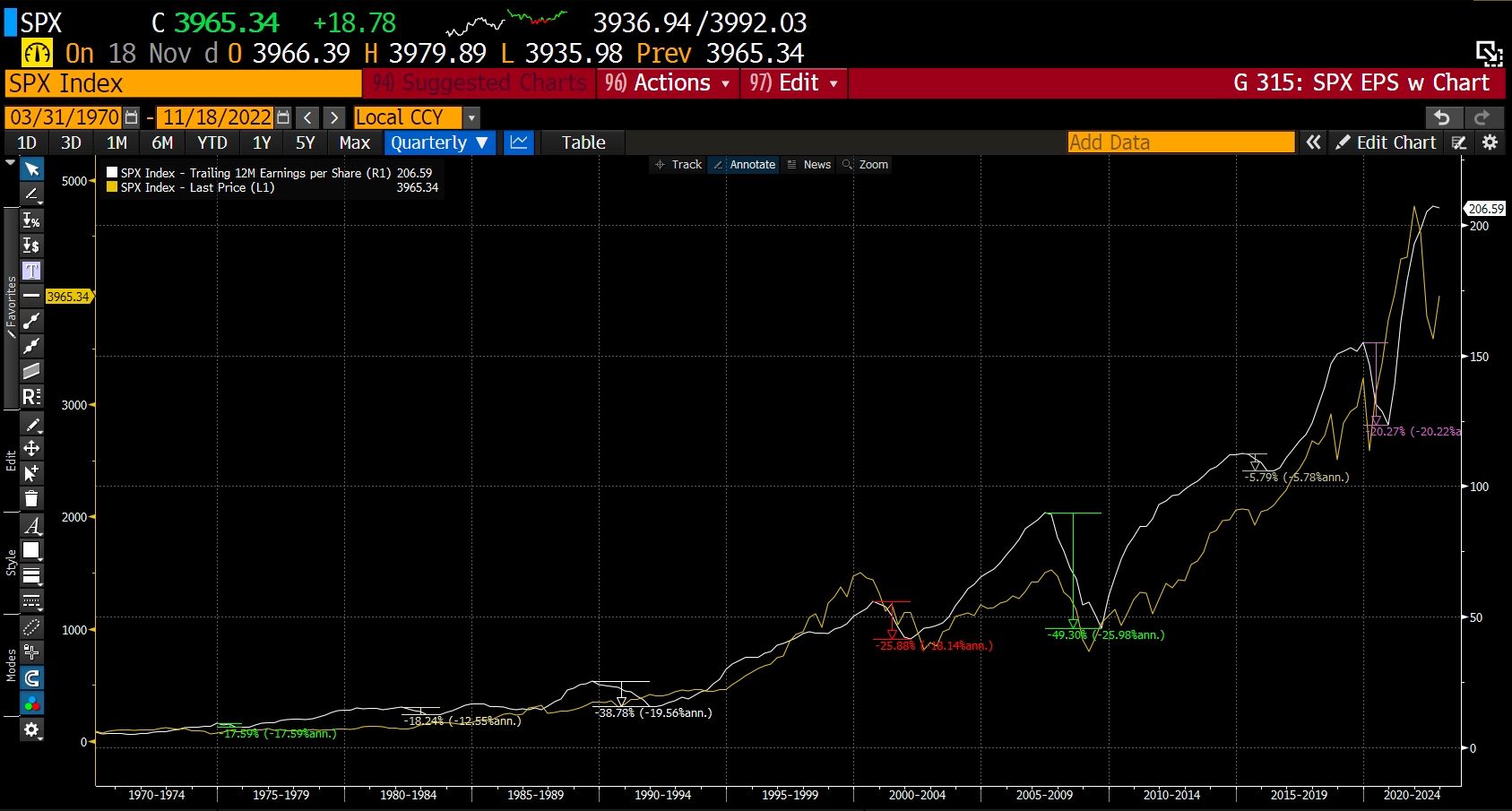

So, what is so interesting about this cycle is that the markets and economy have really weathered quite a bit of turmoil and damage, but has continued to stand. Bubbles have burst and over $30 Trillion dollars of value has been erased from financial assets. This is actually a larger loss of value than the US saw in the Great Financial Crisis of 2008-09! But yet, earnings are still up year over year- amazing. As you see in the graph below, S&P earnings (white line) have only begun to flattten out. For this to be the case this late in a Bear cycle is highly unusual. In the GFC, we saw a 49% drop in earnings and it occurred mostly simultaneous to the market drop.

So, while markets may yet fade this latest rally, there are emerging positives. For long term investors there is once again real opportunity in many asset classes. The FED appears to have gained their footing. The Inflation data is improving. If the economy can continue to be resilient in the face of these shocks then the following recovery will be compelling. There is some light at the end of the tunnel. This will ultimately turn out to yet another opportunity for smart investors to find value when others are focused on all the obvious negatives.

Comments