For the all the tensions in Washington D.C. over who’s the blame for the shutdown of the government, investors are going to be quite happy. A shutdown of government sounds negative but is viewed by investors as a wrinkle rather than a big fork in the road. This is seen from bond and stock returns that have been uniformly positive during and after shut downs and debt ceilings negotiations end. U.S. political risk is seen an investment opportunity and there are several reasons why.

According to a Congressional Research Service report, when a “funding gap” occurs, government agencies start the process of “shutting down” activities and furlough personnel. The debt ceiling is a limit that Congress imposes on how much debt the federal government can carry. When the debt ceiling is reached, the U.S. Treasury must choose between paying government salaries or the interest on Treasury debt.

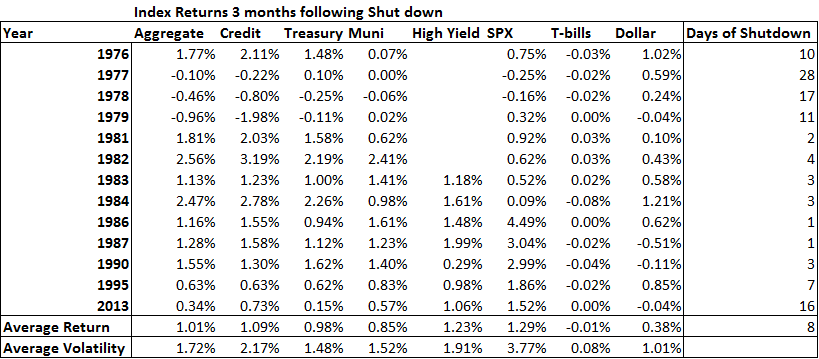

The word “limit” is what markets appreciate. Without a functioning government or ability to issue debt, the economy could be paralyzed. Politicians afraid of the prospect, especially when it affects their polls negatively, come together in the last hour to resolve differences. As markets understand this well, a political debacle causing volatility turns into an opportunity to sell the “political noise.” Index returns show bonds and stocks historically benefit (see Fig.1), regardless how long it took to reopen the government and regardless the extent of political brinkmanship. Now the Senate and House have moved to voted a gap bill to fund the government for 3 weeks, markets have another opportunity by February 8 to “sell the noise.” That is when negotiations about the budget bill that includes politically sensitive issues such as immigration, must be finalized.

Figure 1

Source: Bloomberg Barclays Indices

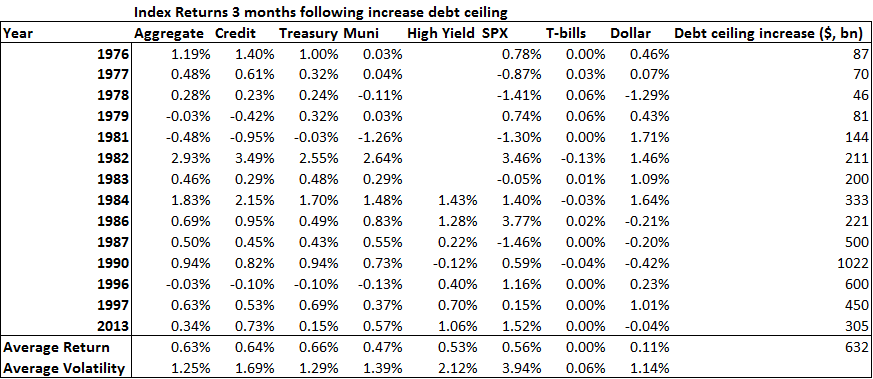

In the past, debt ceilings have been generous to markets as well. In 2011, when the debt ceiling conflict caused S&P to downgrade of the U.S. Treasury debt, financial conditions tightened substantially. A debt ceiling limit or breach is the equivalent of a “technical” default in which the Treasury is unable to issue new debt or service existing debt. Fed researchers found that in a situation of a debt ceiling breach, Treasury Bills are specifically at risk and could cause a financial contagion if it becomes clear the government can’t fulfill near term obligations. This would be enough reason for markets to sell off sharply as they initially did during the debt ceiling impasse in 2011. A reason why markets rebound is that a last minute political resolve allows for government spending to resume and potentially expand to sectors that represent larger parts of the economy. When a debt ceiling becomes a crisis, developments can influence Fed policy that could result in monetary easing. This happened in 2011 when the Fed undertook "operation Twist" after the debt ceiling standoff ended.

Figure 2

Source: Bloomberg Barclays Indices

The history of shut downs and debt ceilings taught investors to not pay too much attention to the noise of headlines. What has become engrained in investor psychology is uncertainty begets certainty and therefore there is always an opportunity to invest. Historically, volatility during shutdowns and debt ceilings has therefore been below long-term average volatility. That has conditioned investors political events are not to be too concerned about. Economic damage from a shutdown has been on average -0.3% of GDP according to Moody’s analytics estimates. Markets view that damage as an opportunity for new fiscal stimulus to come on line to support the economy.

Gearing up for February 8 when negotiation about the budget bill could again face strains, and a debt ceiling that has a drop-dead date, there remains plenty political noise to cause initial concerns among investors. History of returns shows however, there is also plenty of opportunity to reengage capital.

Comments